Create an account

Or Signup with your email

Section 147 of the Income Tax Act, 1961 provides for the reopening of assessment proceedings. This section gives discretion to the Assessing Officer (AO) to reopen the assessment proceedings when he/she has reason to believe that some of the income has escaped assessment.

Every earning individual is required to file the return to the income tax department if the earning is chargeable to tax. The tax authorities examine your income tax return (ITR) and if necessary, they can seek additional clarifications. This process of examining the return of income is referred to as assessment.

For instance, anything you earned in the financial year (FY) 2023-24 is assessed in the assessment year (AY) 2024-25. After self-assessment, the taxpayer will compute the tax liability and will have to pay that amount and file ITR. Thereafter, the income tax department (ITD) conducts preliminary checking of returns for any arithmetical errors, incorrect claims, etc., which is a fully computerised process. At this stage, there is no detailed scrutiny of ITR filed.

A Complete Guide to Reassessment in India

Section 147 of the Income Tax Act, 1961, deals with the reassessment of income by the Income Tax Department. It empowers tax authorities to reopen completed assessments if they have reason to believe that income has escaped assessment. With several amendments in recent years, especially through the Finance Acts of 2021 and 2022, this section has gained significant importance in tax administration and compliance. This blog will help you understand Section 147 in simple language, including the procedure, key terms, and taxpayer rights.

Section 147 grants the Assessing Officer (AO) the authority to assess or reassess income if it is believed that any income chargeable to tax has escaped assessment. This may include cases where no return was filed or where income was under-reported in a previously filed return.

Key Point: This section plays a crucial role in ensuring that all taxable income is brought under the tax net, even after an assessment has been completed.

There are several types of assessments conducted by the Income Tax Department:

The Finance Act, 2021 introduced major changes to Section 147:

Important:The Finance Act, 2022 provided further clarity on these changes and streamlined the reassessment process with defined timelines and procedures.

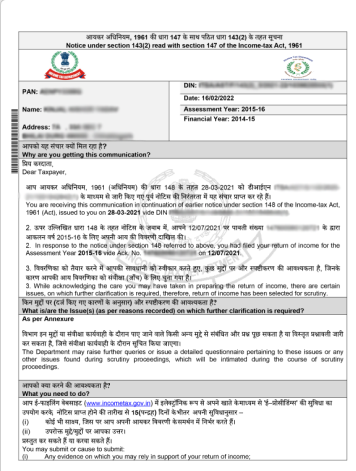

Section 147 works closely with Sections 148 to 153:

| Step | Description | Timeline |

|---|---|---|

| 1 | Preliminary inquiry (Section 148A) | Before issuing notice |

| 2 | Show-cause notice served | Min. 7 days to respond |

| 3 | Approval from higher authority | Mandatory |

| 4 | Notice under Section 148 | Issued after response |

| 5 | Filing of return by taxpayer | Within time given in notice |

| 6 | Assessment completed | Within 12 months from end of FY of notice |

Example: Mr. A files his ITR showing ₹8 lakh income. Later, a large deposit of ₹25 lakh in his bank account is flagged via AIS. The AO initiates inquiry under Section 148A and finds that the source of funds was not explained. AO issues notice under Section 148, and reassessment under Section 147 leads to additional tax demand.

Taxpayers are protected under the law and have the following rights:

Right to be Heard: Taxpayers must be given a chance to explain before reassessment.

Right to Appeal: Orders passed under Section 147 can be challenged before the Commissioner of Income Tax (Appeals), ITAT, and further courts.

Right to Information: The AO must disclose the reasons for reassessment.y

Time Limits: Tax authorities must act within legal time limits, ensuring fairness.

Section 147 of the Income Tax Act is a powerful tool for the Income Tax Department to address tax evasion and bring unreported income under the tax net. However, with recent amendments, the reassessment process has become more transparent and taxpayer-friendly. Understanding this section helps both individuals and businesses stay compliant and protect their rights.

If you're unsure about how Section 147 applies to your case or have received a notice, it’s best to consult a qualified tax professional or CA.

If you receive a notice under Section 147 (or Section 148), follow these steps to respond:

Pro Tip: Always respond within the deadline and maintain polite, factual communication. Ignoring the notice can lead to penalties or even prosecution.

As per the Finance Act, 2021, the time limits for reopening assessments under Section 147 are:

Also, no reassessment can be done after 3 years unless the AO has "evidence-based information" of significant income escaping assessment.

Note: The timelines are strictly enforced to ensure fairness and to protect taxpayer rights.

While Section 147 itself does not impose penalties, reassessment may lead to additional tax, interest, and penalties under related sections if the AO finds unreported income.

Here’s what you could face:

Best Practice: Always declare all income truthfully and keep transaction records to avoid penalties.

Here are the most common triggers that lead to reassessment notices:

The tax department uses AI-powered systems to detect such mismatches and anomalies.

Yes. If you receive a notice under Section 148 (related to Section 147), you must file a fresh income tax return within the time mentioned in the notice. Not responding may lead to best judgment assessment under Section 144 and attract penalties.

Ignoring the notice is never a good idea. Even if you believe your original ITR was correct, you must comply and explain your case properly.

Section 147 of the Income Tax Act itself is not a criminal section — it deals with the reassessment of escaped income. Receiving a notice under Section 147 is not an offense; it’s a compliance opportunity.

However, if during reassessment, it's found that you deliberately evaded taxes, you may face prosecution under Section 276CC or Section 277. In that case:

Key takeaway: Section 147 itself is civil in nature. It becomes criminal only if tax evasion is proved with intent.

This is completely unrelated to the Income Tax Act. Under the Indian Railways Act, 1989, Section 147 pertains to:

Summary:

Objective: To ensure public safety and security by restricting unauthorized entry onto railway property.